At some point in everyone’s life, they will have to choose a FinanceGuider.com to use. When looking for banks, it’s important that they offer the products and services that you need. The two major choices of banks you have include local banks/credit unions vs large banks. So which is the better option?

Like anything in finances, it comes down to your preferences. Both big banks and community banks have their pros and cons. So here is what you should think about when looking at large and community banks.

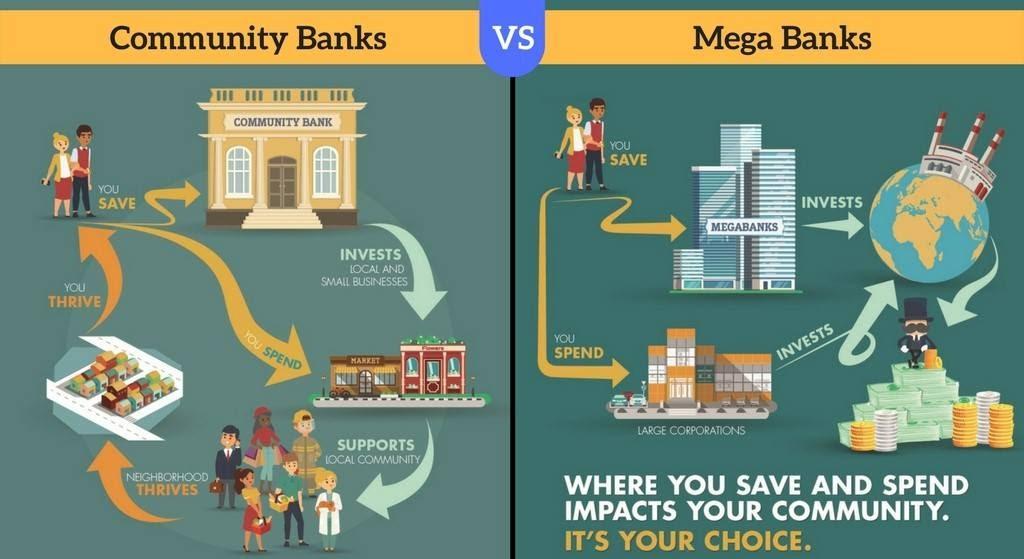

What Is a Community Bank?

Community banks are banks that are owned and operated by people who live in the community they serve. This is in contrast to large megabanks, which are owned and operated by shareholders who may or may not be actually customers of the bank. Community banks are thus typically more in tune with the specific financial needs of their communities and tend to give a more personalized banking experience than a large multinational firm.

Community banks offer the full range of banking products, including checking accounts, savings accounts, loans, credit cards, and more. There are 5,000+ community banks in the US that collectively manage over $3 trillion in assets. Community banks are especially popular in rural areas where large banks may not be present.

Difference Between Community Banks and Large Banks

The main difference between community banks and large banks is who owns them. Community banks typically serve individuals and the bank itself is owned by the customers that use it. Large banks, in contrast, are owned by shareholders that might include large, institutional investors. Large banks tend to have a bigger presence in corporate lending while community banks mostly lend to individual households.

Pros/Cons of Large Banks

Pros

Convenience

One of the best features of using a large megabank is convenience. Megabanks like Bank of America, Wells Fargo, Citigroup, etc. have branches all over the country and serve 10s of millions of customers. If you are a fan of in-person banking, then these large institutions allow you to find every service that you need, whether it’s home loans, bank accounts, or something else. For example, at Wells Fargo, you can open a checking account, savings account, credit card, and investment account, all at the same place. Having these products and services at the same place is streamlined and convenient.

Lots of Products

Large banks usually have a huge list of banking products with a lot of variations. Large banks provide savings accounts, investment accounts, credit cards, home loans, business loans, and other more complicated financial products. Large banks also usually have extensive ATM networks so you can grab your cash wherever you need it.

Cons

Cost

Large banks usually are more expensive for certain products. For example, you often have to pay for a checking account. There might be ways to waive fees by either depositing a certain amount each month or maintaining above a certain balance. Genuine free personal accounts are relatively rare though. In contrast, business checking accounts at large banks are often free.

Not Personalized

Large banks have a lot of products but they usually do not engage with the community the way community banks do. Large banking chains are notorious for being very impersonal and “cold” and they do not have an understanding of a community’s needs as a community bank does. Since large banks are owned by shareholders, their interests do not necessarily lie with the customers who use the bank.

Pros/Cons of Community Banks

Pros

Personalized Services

Community banks operate in local areas and so have a deeper understanding of a given community’s financial needs. You are much more likely to get personalized services that are responsive to your specific conditions at a community bank. Community banks are also owned by the customers so there is much less of a conflict of interest between customers/shareholders.

Work with Individuals

Most community banks work with individual households, not large business entities and conglomerates. As such, a community bank is more likely to make a loan to a moderate-income individual for a house, for example, than a large institution.

Lower Costs

In general, community banks offer lower costs on theri banking products. For example, interest rates for a home loan are likely to be lower at a community bank loan than a one from a large lending institution. Interest fees on credit cards also tend to be lower as well.

Necessary

Very often, community banks might be the only bank that has a physical branch in your location. Large banks do not really have an incentive to set up shop in smaller towns, so sometimes a community bank will be the most readily available option.

Faster Processing

Since community banks do not have as large a clientele as megabanks, there is much less bureaucratic bloat and things can get done faster. That means you are likely to get a loan or other application processed faster at a community bank than a large one.

Cons of Community Banks

Limited Products and Services

Since they are smaller, community banks often offer fewer products and services overall than larger banks. While community banks will have the bases covered and include things like online and mobile banking, you might need to go to a large financial institution to find any specialized products or services.

Smaller Cash Reserves

Community banks may also be limited by how much cash they have on hand. That means you might not be able to get a loan for the amount that you want if it is too high. For example, if you were trying to get a small business loan, your community banks may not be able to supply it if you

Conclusions

Both community banks and megabanks have their pros and cons. At the end of the day, the right choice depends on your needs and preferences. That being said, if you are in the middle of switching from a large bank, we would recommend looking into community banking,

Comments are closed.