By Greg Ahuy – April 8, 2021

In this article, we will take a look at the risk allocation under the PPA.

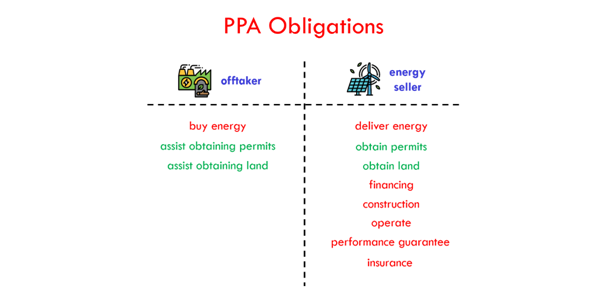

In the previous article on the PPA, we focused on energy sales under the PPA, and briefly reviewed the obligations of the off-taker and energy seller concerning the energy sales.

The off-taker has an obligation to purchase the committed energy production during the term of the PPA.

While the energy seller has an obligation of generating and delivering the committed energy production.

The energy purchase and sale are the main obligations of the off-taker and energy seller.

The PPA, however, includes additional obligations apart from energy purchase and sale, especially for the energy seller.

Since the project will be built from scratch, the energy seller will also be responsible for obtaining all necessary permits and land for the project.

Sometimes, this obligation related to permits and land can be shared with the off-taker, especially in emerging markets, where the off-taker is usually a government-owned entity.

Next, the energy seller is responsible for arranging financing, construction, and operation of the project, including the construction of interconnection facilities.

Note that such events as getting all necessary permits, reaching financial close, starting and ending construction, and beginning operations will be defined as project milestones in the PPA and will have specific dates. Failing to achieve these milestones will, typically, result in the default of the PPA with important negative consequences for the energy seller.

Energy seller is obliged to maintain necessary performance guarantees and insurance policies during the construction and operation of the project.

The obligation of the parties under the PPA, create and allocate the project risks between the parties.

For example, since it is the obligation of the off-taker to purchase the committed energy production during the term of the PPA, the off-taker takes the energy price and volume risks.

The price risk is the risk that energy prices may be lower in the future than the PPA fixed price.

Volume risk is the risk that the energy bought under the PPA may not be necessary, however, the off-taker has to, still, pay the energy seller.

In addition to the price and volume risk, in emerging markets, the off-taker takes the risk of adverse currency movements, political and regulatory risks and the risks arising out of Force Majeure Events.

When it comes to the risks allocated to the energy seller, they include risk associated with construction, operation performance, energy delivery risk, and resource variability risk.

Since both the off-taker and the energy seller take on significant risk under the PPA, each party wants the other to be creditworthy.

Typically, in the developed markets, the off-taker is an investment-grade utility, which is sufficient to mitigate the counterparty risk.

While for the off-taker in the emerging markets, various credit enhancing mechanisms may be available such as sovereign guarantees from the government, partial risk guarantees, and political risk insurance.

Energy seller is required to post a performance bond to enhance its creditworthiness, which comes, typically, in the form of a letter of credits or bank guarantees.

Sponsor support agreement, which represents guarantees from the seller’s equity investors, may also be required. These are guarantees that additional funding will be provided by the investors in case there is a funding shortfall, for example, due to construction costs overruns.

Seller is also required to set up and maintain a security cash fund, that the off-taker can draw on to cover the penalties payable by the energy seller.

And, finally, the energy seller is required to acquire and maintain appropriate insurance during the construction and operation of the project.

In this article, we learnt about the debt service reserve account in project finance transactions. To learn about financial modelling for project finance please enroll in our courses:

Project Finance Modeling for Infrastructure Assets – https://www.financialmodelonline.com/p/project-finance-modeling-course

Project Finance Modeling for Renewable Energy – https://www.financialmodelonline.com/p/project-finance-modeling-for-renewable-energy

Advanced Financial Modeling for Renewable Energy (US Market) –https://www.financialmodelonline.com/p/advanced-financial-modeling-wind-solar

Comments are closed.